Changes to scorecard

What changed and how it affects me & my company

On 9 April 2019, the Minister of Trade and Industry signed four amendments to the Amended Generic B-BBEE Codes of 2013. These amendments were gazetted on Friday 31 May 2019 and will come into effect on 31 November 2019

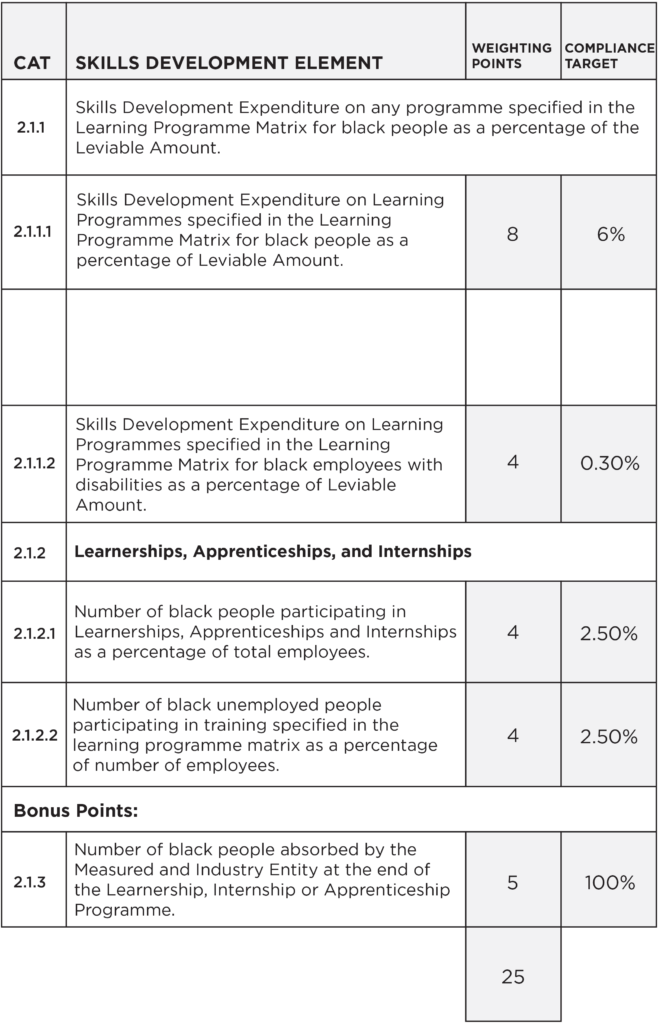

How it worked

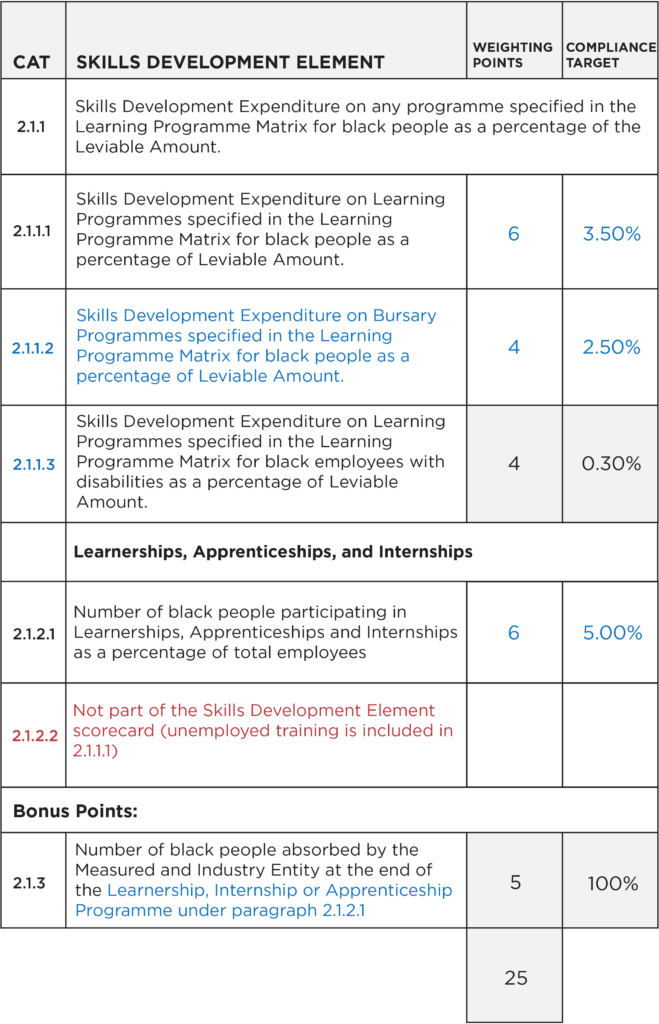

How it works now.

Government Gazette Vol. 647 31 May 2019 No. 42496

Key measurement principles

The following criteria must be fulfilled in order for the Measured Entity to receive points on the Skills Development Element scorecard:

- The 3.5% compliance target under paragraph 2.1.1.1 includes external training expenditure for unemployed black people.

- Initiatives implemented under paragraph 2.1.1.1 cannot be counted under paragraph 2.1.1.2.

- A trainee tracking tool has to be developed in order for the Measured Entity to score under paragraph 2.1.3

Outcome:

- The Entity must achieve a minimum of 40% of the total weighting points EXCLUDING BONUS points (40% of the 20 points i.e. 8 points).

General Principles

- Skills Development Expenditure arising from Informal and workplace Learning Programmes, or from Category F and G under the Learning Programmes Matrix represent 25% (previously 15%) of the total value of Skills Development Expenditure.

- Training costs such as accommodation, catering, travelling, SDF or training Manager does not apply to Skills Development Expenditure recognised in paragraph 2.1.1.2.

- Stipend linked to a bursary programme in terms of 2.1.1.2 constitute Skills Development Expenditure.

- Mandatory training i.e Health and Safety does not qualify as Skills Development Expenditure.